Working Capital Credit Protocol for ONDC 2024

ONDC (Open Network for Digital Commerce) is a government-backed initiative aiming to democratize and standardize digital commerce, including financial services, by creating an open, interoperable network. In collaboration with ONDC, Bizongo acted as a tech partner to streamline working capital lending for India's MSMEs.

ROLE

Product Designer

SECTOR

FinTech

TEAM

Aishwarya Bindana, Srishty Banga, Abbas Dawood

OVERVIEW

MSMEs in India is an industry historically plagued by fragmentation and inefficiencies. This initiative focused on building a credit protocol that digitized and simplified loan access, ensuring seamless transactions between lenders and borrowers while reducing friction in documentation and compliance.

IMPORTANT TERMS

MSME (Micro, Small & Medium Enterprises): Businesses classified based on investment and turnover, crucial to India's economy.

Working Capital Loans: Short-term funds used to manage daily operational expenses.

Credit Protocol: A standardized digital framework enabling lenders and borrowers to transact efficiently.

PROBLEM

India’s MSME sector faces a huge credit gap due to fragmented financial systems, complex documentation,

and limited digital lending guidelines.

and limited digital lending guidelines.

Traditional lenders hesitate to fund MSMEs due to high underwriting costs, pushing businesses toward informal, high-interest loans. The ONDC Credit Protocol was developed to standardize and digitize working capital lending, making loan access seamless while reducing risks for lenders.

Know more details here

Our main constraint was speed—we needed to develop and deploy the protocol quickly to secure a first-mover advantage in digitizing MSME lending before competitors could establish similar frameworks.

IMPACT

1. Reduce Loan Processing Time

Borrower application turnaround time aimed to drop from

60 days to under 2 hours through standardized documentation and structured workflows.

Borrower application turnaround time aimed to drop from

60 days to under 2 hours through standardized documentation and structured workflows.

2. Higher Borrower Approval Rates

By streamlining document collection and underwriting, approval rates set to increase by 35%, improving MSME access to formal credit & reduction on bad-matches.

By streamlining document collection and underwriting, approval rates set to increase by 35%, improving MSME access to formal credit & reduction on bad-matches.

3. Faster Lender Decision-Making

Pre-fetched data and structured submissions to cut lender evaluation time by 50%, reducing delays in offer generation.

Pre-fetched data and structured submissions to cut lender evaluation time by 50%, reducing delays in offer generation.

4. Expanded Access to Credit

MSMEs could apply to multiple lenders simultaneously, increasing their chances of securing funding without redundant applications.

MSMEs could apply to multiple lenders simultaneously, increasing their chances of securing funding without redundant applications.

RESEARCH METHODS

To develop a well-rounded and effective credit protocol, we conducted extensive industry and UX research, combining qualitative and quantitative methods to capture diverse perspectives:

1. Active Collaboration with ONDC

Conducted stakeholder interviews and workshops with their network

of lenders and borrowers to understand real-world lending workflows, roadblocks, and regulatory constraints.

Conducted stakeholder interviews and workshops with their network

of lenders and borrowers to understand real-world lending workflows, roadblocks, and regulatory constraints.

2. Engaging with Bizongo's Network of Lenders

Used expert interviews and contextual inquiry to study underwriting practices, risk assessment models, and operational challenges in approving credit.

Used expert interviews and contextual inquiry to study underwriting practices, risk assessment models, and operational challenges in approving credit.

3. Competitor Analysis

Researched existing lending solutions to identify best practices, gaps, and opportunities for differentiation, ensuring our protocol was both innovative and practical.

4. Consulting Bizongo's Borrower Base

Deployed user interviews and surveys to gather insights on MSME pain points, accessibility issues, and friction in existing loan application processes.

Deployed user interviews and surveys to gather insights on MSME pain points, accessibility issues, and friction in existing loan application processes.

5. Analyzing Bizongo’s Internal Historical Data

Leveraged quantitative research, data analysis, and trend mapping to identify inefficiencies, lending behaviors, and system-wide bottlenecks.

Leveraged quantitative research, data analysis, and trend mapping to identify inefficiencies, lending behaviors, and system-wide bottlenecks.

IMPORTANT INSIGHTS

Some main insights that shaped the course of the user flow and design decisions.

FOR BORROWERS

1. Lack of Standardization

No uniformity in documentation requirements across financial institutions, with document demands ranging from 12 to 40

depending on the lender.

2. Lengthy & Unclear Process

No consolidated list of required documents or steps; banks request documents in batches, causing delays. On average, the process took

60 days on our system.

3. Limited Access to Documents

Borrowers frequently rely on CAs for document retrieval, leading to

high turnaround time (TAT) due to back-and-forth exchanges.

4. Repetitive Applications

No way to apply once and reach multiple lenders—borrowers must

go through the entire process separately for each financial institution.

No uniformity in documentation requirements across financial institutions, with document demands ranging from 12 to 40

depending on the lender.

2. Lengthy & Unclear Process

No consolidated list of required documents or steps; banks request documents in batches, causing delays. On average, the process took

60 days on our system.

3. Limited Access to Documents

Borrowers frequently rely on CAs for document retrieval, leading to

high turnaround time (TAT) due to back-and-forth exchanges.

4. Repetitive Applications

No way to apply once and reach multiple lenders—borrowers must

go through the entire process separately for each financial institution.

FOR LENDERS

1. Unreliable Data & Documents

Issues with document authenticity and credibility, increasing risk.

2. Fragmented Document Submission

Documents arrive in batches rather than all at once, making evaluation cumbersome.

3. Complex Underwriting Processes

Lenders rely on multiple internal checks, making the approval process slow and inefficient.

4. No Real-Time View of Borrower Liabilities

Borrowers may receive loans from multiple lenders simultaneously,

but CIBIL updates only after a month, leading to over-financing risks.

Issues with document authenticity and credibility, increasing risk.

2. Fragmented Document Submission

Documents arrive in batches rather than all at once, making evaluation cumbersome.

3. Complex Underwriting Processes

Lenders rely on multiple internal checks, making the approval process slow and inefficient.

4. No Real-Time View of Borrower Liabilities

Borrowers may receive loans from multiple lenders simultaneously,

but CIBIL updates only after a month, leading to over-financing risks.

MAPPING ON THE GO

As we raced against the clock, we created an iterative user journey map in parallel to gathering insights, ensuring our design decisions were informed by real-time learnings and continuously evolving.

ALL HAIL DESIGN SYSTEMS

To accelerate execution, we bypassed the low-fidelity stage and directly built high-fidelity designs using our trusty design system, Bamboo—enabling us to deliver in just 12 days.

To accelerate execution, we bypassed the low-fidelity stage and directly built high-fidelity designs using our trusty design system, Bamboo—enabling us to deliver in just 12 days.

This allowed us to seamlessly pick up primitives and

components, rapidly assembling the protocol’s UI without sacrificing quality or consistency.

components, rapidly assembling the protocol’s UI without sacrificing quality or consistency.

Pre-defined components and micro-interactions from our design system

SOLUTIONING

For each challenge, we used a structured Hypothesis → Strategy → Solution

framework to ensure clarity and effectiveness.

For each challenge, we used a structured Hypothesis → Strategy → Solution

framework to ensure clarity and effectiveness.

1. Lack of Standardization & Fragmented

Documentation Submission

Documentation Submission

Hypothesis

The absence of a unified document framework forces lenders and borrowers into an inefficient cycle, increasing approval times.

The absence of a unified document framework forces lenders and borrowers into an inefficient cycle, increasing approval times.

Strategy

Establish a standardized application structure in collaboration with ONDC, ensuring all lenders follow a common framework for required documents and steps.

Establish a standardized application structure in collaboration with ONDC, ensuring all lenders follow a common framework for required documents and steps.

Solution

Identify common mandatory documents across lenders for basic underwriting. For lender-specific requirements, request only decision-critical documents separately, streamlining the process while maintaining lender flexibility.

Identify common mandatory documents across lenders for basic underwriting. For lender-specific requirements, request only decision-critical documents separately, streamlining the process while maintaining lender flexibility.

Reduced the number of necessary documents from 20+ to 5 for preliminary underwriting

2. Lengthy, Unclear Process & Complex Underwriting

Hypothesis

Borrowers drop off due to a lack of visibility into the process, while lenders face delays due to manual reviews and scattered information.

Hypothesis

Borrowers drop off due to a lack of visibility into the process, while lenders face delays due to manual reviews and scattered information.

Strategy

Redesign the borrower experience to make the process clear,

structured, and incentivized, while also reducing lender workload through pre-fetched data.

Redesign the borrower experience to make the process clear,

structured, and incentivized, while also reducing lender workload through pre-fetched data.

Solution

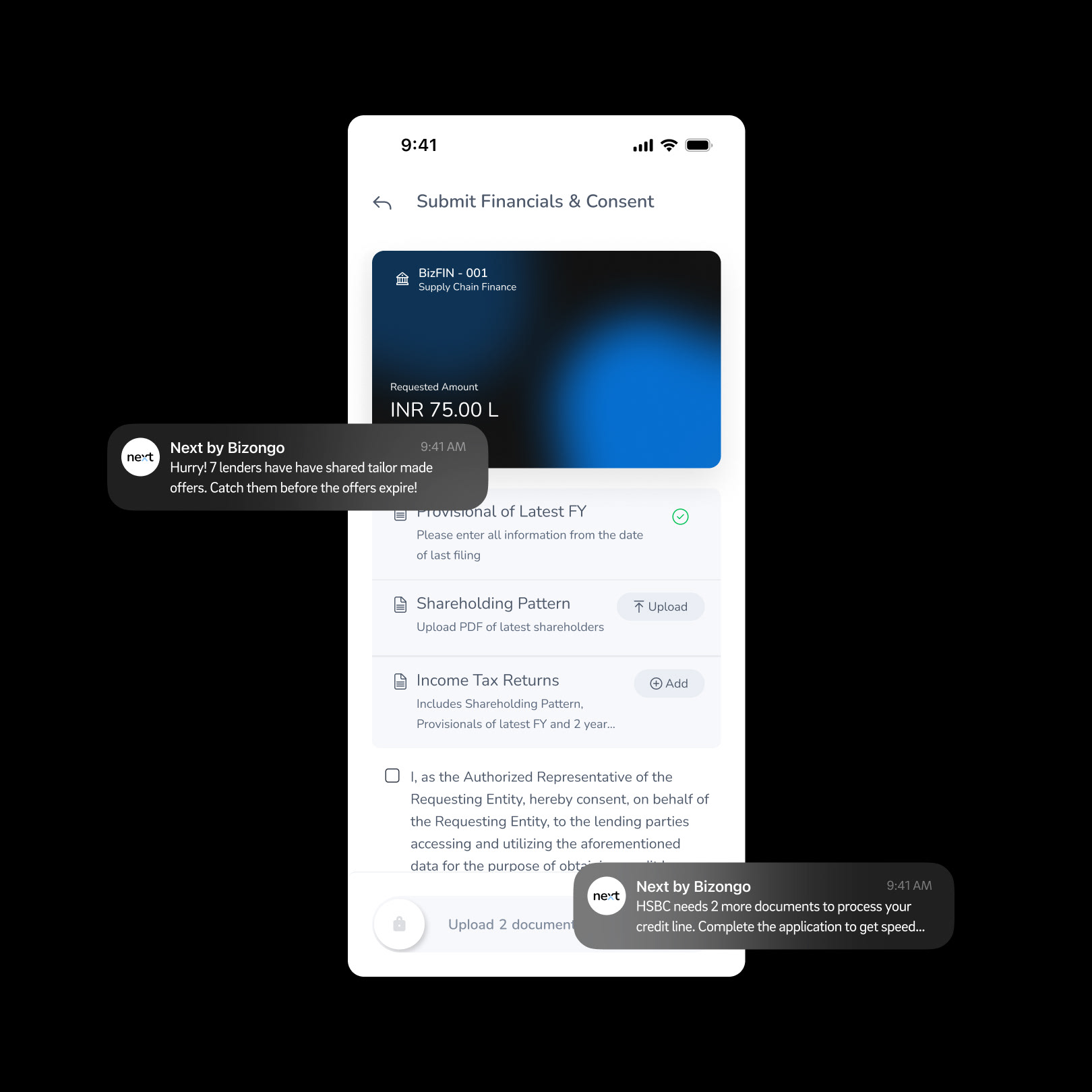

• Introduce a guided application flow with progress indicators

and gamification to keep borrowers engaged.

• Introduce a guided application flow with progress indicators

and gamification to keep borrowers engaged.

• Provide real-time status updates and estimated TATs for each step.

• Mandate lenders to review applications within a fixed time

frame, ensuring faster processing.

frame, ensuring faster processing.

• Pre-fetch critical financial and compliance data to minimize manual underwriting steps for lenders.

Stepper approach to guide the user with a real-time estimate of time taken

Inform the user about the requirements of the process in advance to cut TAT

Subtle hooks to entice users to complete the flow in one go

3. Limited Access to Documents & Data Authenticity

Hypothesis

Borrowers face delays retrieving documents from CAs, and lenders struggle with unreliable data.

Hypothesis

Borrowers face delays retrieving documents from CAs, and lenders struggle with unreliable data.

Strategy

Minimize manual uploads by integrating trusted data sources,

ensuring authenticity and reducing turnaround time.

Minimize manual uploads by integrating trusted data sources,

ensuring authenticity and reducing turnaround time.

Solution

• Fetch documents directly from government-verified sources

(GSTN, banks, MCA, CIBIL, UIDAI, Digilocker, etc.) through APIs instead of relying on borrower uploads.

• Fetch documents directly from government-verified sources

(GSTN, banks, MCA, CIBIL, UIDAI, Digilocker, etc.) through APIs instead of relying on borrower uploads.

• Allow different users (CAs, co-founders, finance teams) to contribute to the application without dependency on a single person.

• Enable seamless digital sharing of documents to remove the need for offline communication and reduce processing time.

Pre-fetch company data to provide to the lenders

Enable users to share certain steps which need to be completed by another persona

Allow users to fetch authentic data from government sources in one click

4. Repetitive Applications Across Lenders & No Real-Time

Borrower Liabilities

Hypothesis

Borrowers waste time applying to multiple lenders separately,

and lenders lack real-time visibility into borrower liabilities, leading

to over-financing risks.

Borrower Liabilities

Hypothesis

Borrowers waste time applying to multiple lenders separately,

and lenders lack real-time visibility into borrower liabilities, leading

to over-financing risks.

Strategy

Create a broad-based application system where borrowers can apply once and get offers from multiple lenders, while ensuring lenders see borrower commitments in real time.

Create a broad-based application system where borrowers can apply once and get offers from multiple lenders, while ensuring lenders see borrower commitments in real time.

Solution

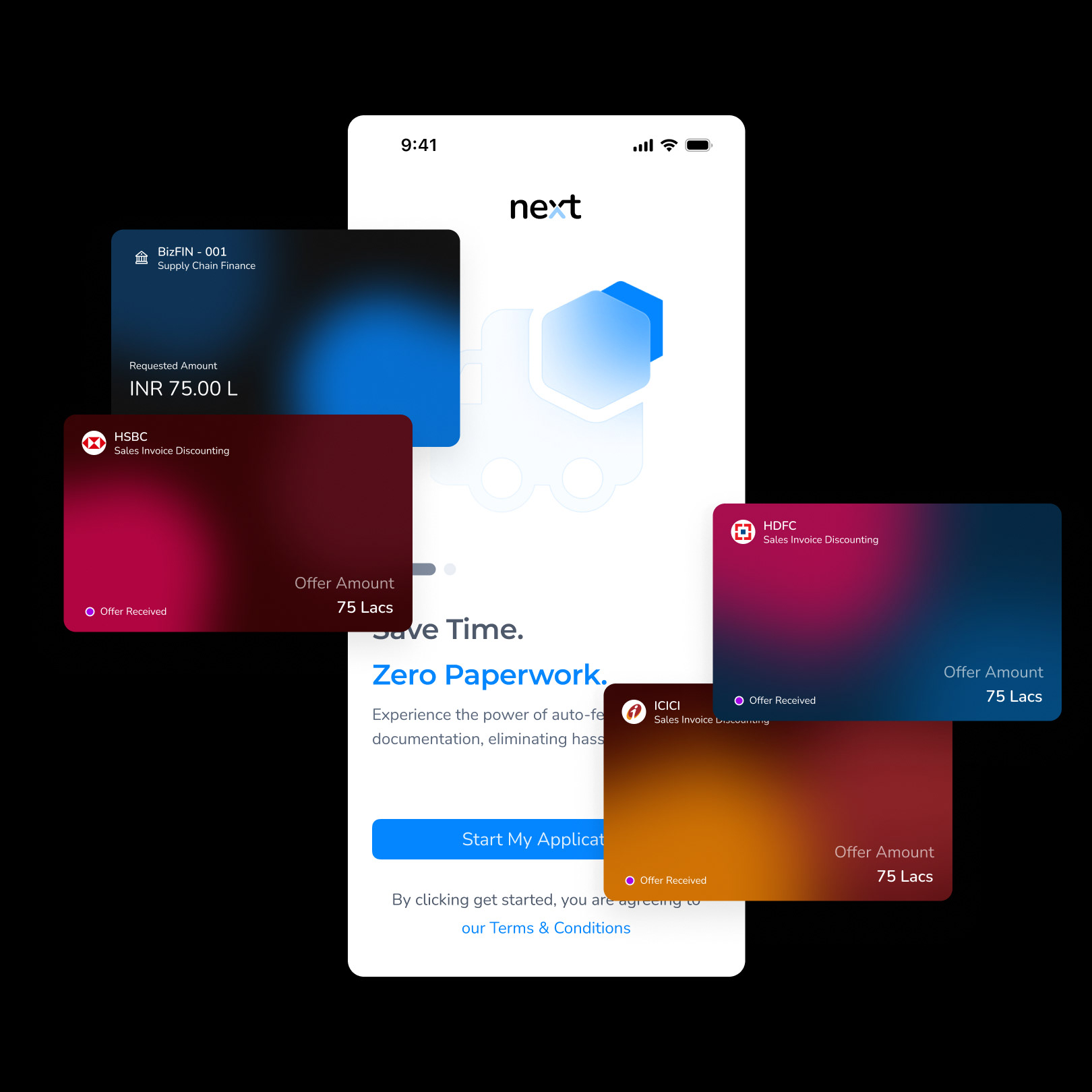

• Democratize the application process by displaying all lenders

on the ONDC network along with their general acceptance criteria.

• Democratize the application process by displaying all lenders

on the ONDC network along with their general acceptance criteria.

• Allow lenders to provide basic conditional offers before full underwriting, reducing unnecessary rejections.

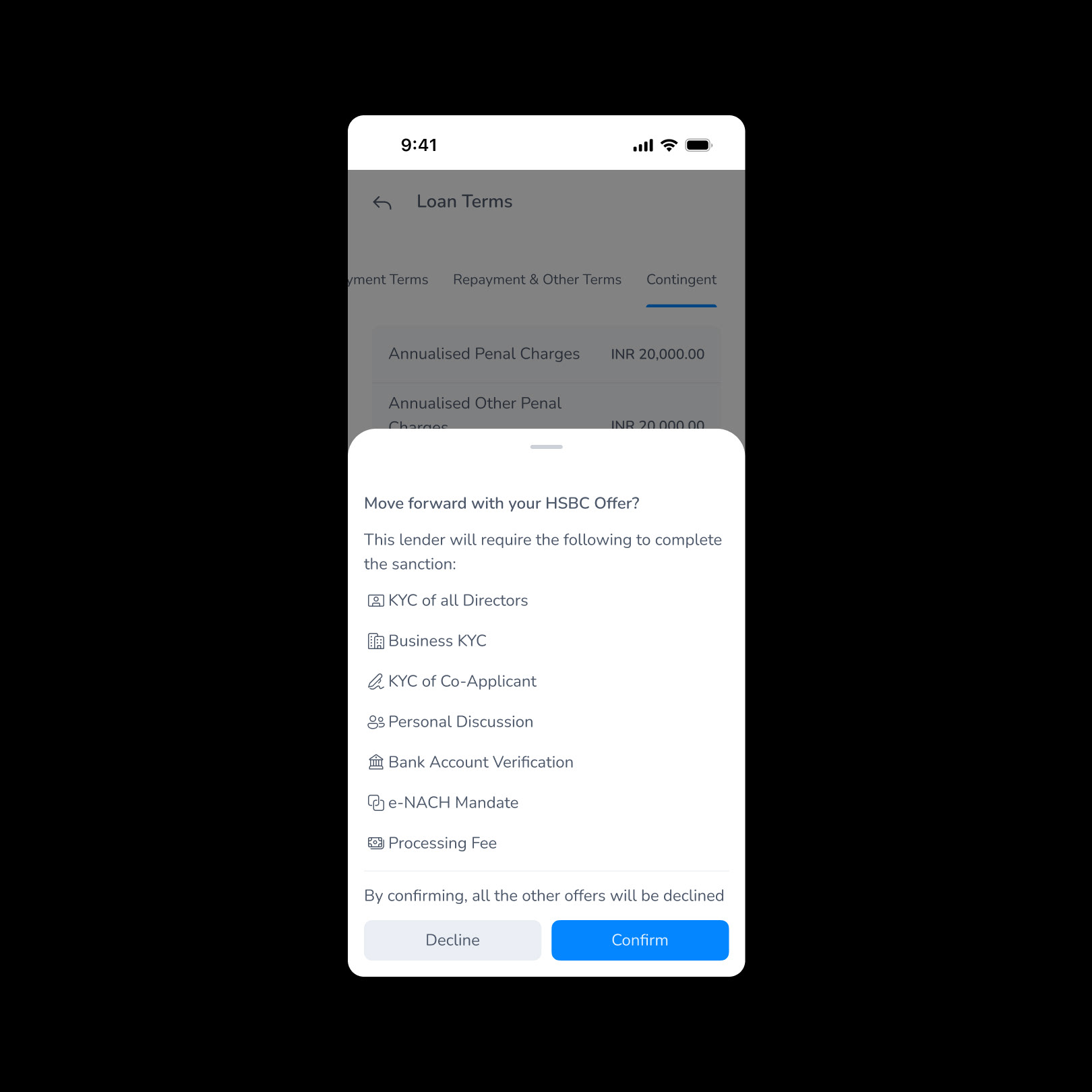

• Block borrowers from accepting multiple loan offers at once to

prevent over-financing risks.

prevent over-financing risks.

Give users the chance to choose from between different lenders with tentative offers

NEXT STEPS

The ONDC Credit Protocol is currently under active testing with ONDC, with real-world validations underway. It has been very well received by the lending and MSME community, who see it as a game-changer in standardizing and streamlining digital lending. Feedback from early testing is being incorporated to further optimize borrower-lender interactions and system performance.

For more details, click here